Building on the panoramic view of the cross-border talent movements landscape in our previous article , this article explores the apportionment of employment income for tax residents in Hong Kong and Mainland China when they work in both regions within a tax year.

Hong Kong

Hong Kong adopts the territoriality basis of taxation, which means that only income sourced in Hong Kong is subject to taxation, whereas income that derives from a source outside Hong Kong by a local resident is, in most cases, not taxed in Hong Kong. This regime will eliminate the occurrence of double taxation of the same income in two or more tax jurisdictions.

The salary tax charging provision of the Inland Revenue Ordinance (Cap.112) (” IRO “), section 8(1A)(a), specifically includes annual leave pay for the purpose of calculating income tax, whereas Section 8(1A)(c) excludes from the salary tax income base the employment income derived outside Hong Kong. Hence, how the leave days in apportionment cases are accounted for will become the key for the actual double tax relief available.

The Court of Appeal has recently taken a closer look at this provision. In this case, an employee, Mr. Lo, worked for a Hong Kong employer and was seconded to China whilst his home employment remained with Hong Kong. As his employment is based in Hong Kong, his salary is chargeable to salaries tax. Given that the conditions for relief from double taxation under the exclusion provision of s.8(1A)(c) of the IRO are satisfied, not all of the employee’s income is chargeable to salaries tax in Hong Kong. What is the proper and fair way to apportion his income in the absence of contractual allocation?

The Court of Appeal has considered four different methods of time-based apportionment, namely:

- Excluding only days worked outside Hong Kong – the days on which the taxpayer worked outside Hong Kong (” non-HK work days “) are identified and only the income apportionable to those days is excluded, which is the primary position advanced on behalf of the Inland Revenue Department (” IRD “) in the Court of Appeal;

- Including only days worked in Hong Kong – the days on which the taxpayer worked in Hong Kong (” HK work days “) are identified, and the income apportionable to all the other days is excluded, which is the formula adopted by the Board of Review on appeal by the employee;

- Excluding days spent outside Hong Kong, whether working days or not – the days on which the taxpayer spent outside Hong Kong, whether working days or not, are identified and the income apportionable to these days is excluded, which is the “day in, day out formula” that has been applied by the IRD in practice; or

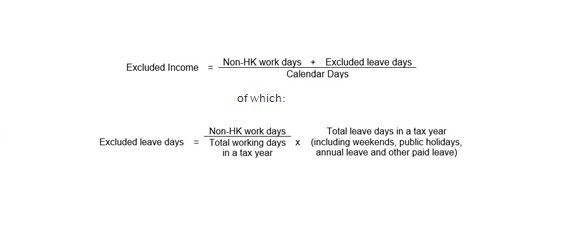

- Excluding days worked outside Hong Kong together with agreed or a proportionate amount of leave days – the non-HK work days are identified, together with the paid leave days attributable thereto, and the income apportionable to these days in aggregate is excluded, which is the IRD’s alternative formula on the appeal as well as the position advanced by the advocates to assist the court.

The Court of Appeal has looked into the results produced by each of the four methods as follows:

- the first approach discounts any leave pay accrued by the taxpayer even though such leave pay may have been attributable to his non-HK work days, and is therefore neither just nor fair;

- the second approach is wrong in principle because it works against the legislative intent, namely that section 8(1A)(c) is an exclusionary provision;

- the third, “day in, day out formula” is not ideal as it could lead to anomalies, depending on where the employee decided to spend his weekends and holidays; and

- the fourth approach is to be preferred as, although the taxpayer does not render services on leave days, the pay on leave days is in reality a reward to the employee for the services which he renders on non-HK work days. As such, leave pay should be taken into account for the purpose of exclusion under section 8(1A)(c) and the question of apportionment will depend on each case as to what services the leave pay in question is attributable. In the absence of any contractual arrangement or any evidence suggesting to what services the leave pay in question is attributable, the Court has approved the following formula for apportionment:

In short, double taxation relief is available in Hong Kong and leave pay attributable to non-HK work days would count towards non-HK income for the purpose of exclusion.

Mainland China

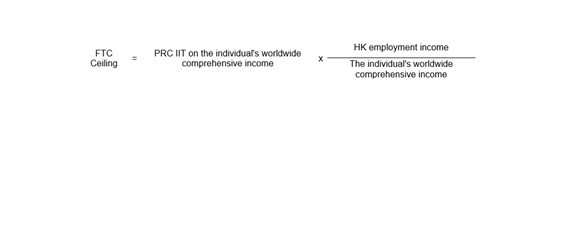

For Mainland tax residents who receive employment income from Hong Kong, in addition to paying Hong Kong salaries tax, they are still subject to PRC individual income tax (” IIT “) on their worldwide income. However, they are eligible to offset the salaries tax paid in Hong Kong as foreign tax credit (” FTC “), subject to a ceiling.

The calculation of FTC ceiling in such a case is set out in the Announcement on Individual Income Tax Policy Concerning Overseas Income issued by the State Taxation Administration and the Ministry of Finance on 17 January 2020, as follows:

Conclusion

For the apportionment/exclusion of non-local income for HK salary tax, the Court of Appeal decision contemplates that employers and employees may agree on how leave pay should be allocated. Therefore, it is advisable for the parties to document such apportionment instead of leaving the matter with the IRD or the Court. In the absence of such agreement, the new approach seems more fair compared to the “day in, day out formula” applied by the IRD previously.

In any event, employees and employers are reminded to keep proper and complete records including the number of leave days taken, the nature of such leave days (if relevant), as well as where the employees have spent his or her working days.

If you have any queries, please feel free to reach out to your usual Withers contacts or to Winnie Weng or Joyce He .